OSAM Research: Dividend Yield vs. Dividend Growth

By OSAM Research TeamSeptember 2012

Investor demand for high-yielding companies has grown even stronger because of the perception that these companies are more defensive and recent news that the Federal Open Market Committee (FOMC) has extended its forecast of low rates until 2015. We believe buying a portfolio of high-quality, global, market-leading companies with superior valuations and high dividend yields provides investors with an excellent opportunity to consistently beat the market,1 while providing high income relative to fixed income securities in the current environment. However, despite the abundance of literature showing dividend yield as a powerful driver of total return over time — accounting for approximately 40 percent of the total return of the S&P 500 since 1926 — there are those who believe high dividend payments are a poor indicator of a company’s future growth prospects and prefer to select stocks using dividend growth instead. Our research confirms that investors should focus on dividend yield rather than dividend growth rates.

Dividend Yield & Dividend Growth

Dividend yield is calculated as the latest dividend payment (annualized) divided by price. We define dividend growth as the rate of change or slope of dividends paid by a company over the most recent three-year period. Our research shows that high dividend yields are a strong indicator of future outperformance. Paying a dividend forces management to invest cash flow only in opportunities with the most optimal risk/reward tradeoff. An example of a stock with a high dividend yield is Eli Lilly (4.2 percent as of 9/20/12), which ranks in the top decile of companies in the U.S. All Stocks Universe.

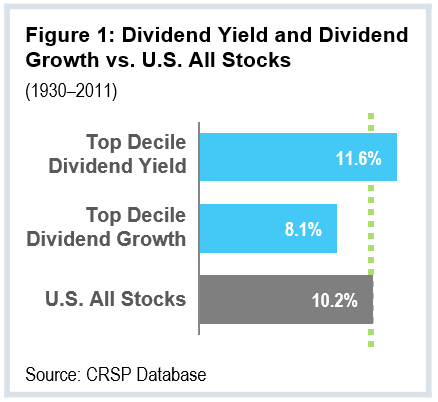

Using data from the Center for Research in Security Prices (CRSP) going back to 1930, we grouped the universe into deciles by dividend yield and dividend growth. In 80+ years — from 1930 to the end of 2011 — the top decile of stocks by dividend yield and dividend growth returned 11.6 percent and 8.1 percent, respectively. During that same period, the top decile by dividend yield handily beat U.S. All Stocks by 1.4 percent annualized, whereas the top decile of dividend growers underperformed annually by 2.1 percent (see Figure 1).

We not only look at returns when evaluating stock selection factors, but are also concerned with how consist-ently a factor beats its benchmark. Since 1930, the top decile of dividend yield outperformed U.S. All Stocks in 71 percent of 924 rolling five-year periods (658 won, 266 lost) versus a win rate of 20 percent for the highest dividend growers in all five-year time frames. The rate of outper-formance increased to 77 percent in rolling 10-year periods for high-yielding names while the win rate for the highest dividend growers fell to14 percent. Finally, the Sharpe Ratio of the highest-dividend-paying stocks was 0.33, vastly better than the 0.15 offered by the top dividend growers.

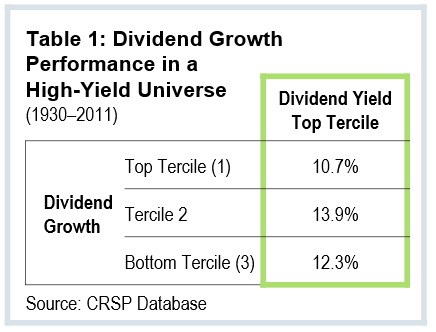

Another interesting point of analysis is to observe how dividend growth performs among companies that pay the highest yields. Again using the CRSP data, we separate the universe into terciles2 based on dividend yield and dividend growth. Table 1 illustrates that investors are not compensated by purchasing stocks with the highest dividend growth rate in a high-yield universe. The highest-dividend-growth stocks underperformed the lowest dividend growers by 1.6 percent.

Global Performance

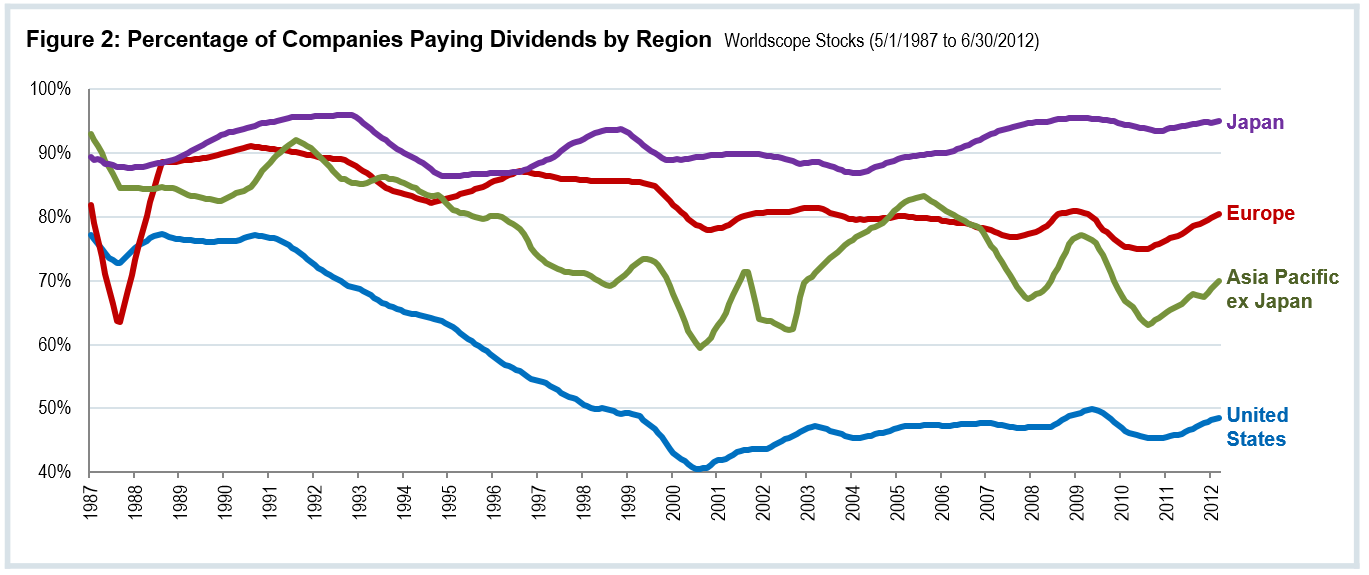

Clearly, dividend yield is superior to dividend growth rates for selecting stocks in the U.S. However, it is our belief that investors must seek yield globally in order to gain a wider opportunity set as U.S. companies have shifted to repurchasing shares as a way to return capital to their shareholders.3 Since the enactment of the Safe Harbor Rule in 1982, which removed many restrictions for share buybacks, the percentage of companies in the U.S. paying a dividend has fallen dramatically. Conversely, the percentage of companies paying a dividend in Asia and Europe far exceeds that of the U.S. (see Fig. 2) — a trend that we expect to remain intact for the near future.

To perform analysis in global markets, we utilize the Worldscope database to build decile portfolios for dividend yield and dividend growth dating back to 1990. In the 22 years from 1990 to 2011, the top decile of stocks by dividend yield returned 14.8 percent (see Figure 3) with a Sharpe Ratio of 0.66. The top decile of dividend growth stocks did not fare nearly as well, and returned 10.0 percent with a 0.38 risk-adjusted return. During the same timeframe, both factors easily beat the Worldscope All Stocks return of 6.9 percent, but dividend yield is the superior factor on an absolute and risk-adjusted basis. Finally, dividend yield is far more consistent and beat the benchmark in 100 percent of 203 rolling five-year periods, while dividend growth had a win rate of 80 percent in five-year timeframes.

Conclusion

Historical precedent clearly demonstrates that investors are better served by focusing on high dividend-yielding companies rather than high dividend growers. The reasons for selecting stocks using dividend yield are two-fold:

- Paying a dividend forces discipline on the management of firms to invest only in the most profitable projects.

- With fixed income yields at historical lows (10-Year Treasury yielding 1.74 percent), high-yielding stocks fill a glaring need for income in many investor portfolios.

The primary reason to avoid high dividend growers: investor pressure for these companies to continue growing dividends at a high rate is unrealistic. This ultimately causes underperformance as dividend growth rates revert. Additionally, rather than focusing solely on a domestic universe when seeking income, we believe investors should focus on a much larger universe of stocks that extends beyond the U.S.

The O’Shaughnessy Enhanced Dividend® strategy seeks large, stable, well-priced stocks with high dividend yield, which is one way for investors to own such well-known companies as Deutsche Telekom, Eli Lilly, AstraZeneca, and Lockheed Martin. Utilizing this strategy can enable investors to benefit from a factor that has proven to perform consistently and with less risk, when backtested through a variety of market cycles.

Footnotes:

1 See “Enhanced Dividend® Commentary” http://www.osam.com/pdf/commentary_jun12.pdf

2 Terciles eliminate clustering that occurs in deciles and quintiles.

3 See “Why U.S. Investors Should Look Beyond Dividend Yield” http://www.osam.com/pdf/commentary_mar12.pdf

General Legal Disclosure/Disclaimer and Backtested Results

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this presentation, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for any portfolio. Gross of fee performance computations are reflected prior to OSAM’s investment advisory fee (as described in OSAM’s written disclosure statement), the application of which will have the effect of decreasing the composite performance results (for example: an advisory fee of 1% compounded over a 10-year period would reduce a 10% return to an 8.9% annual return). Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this presentation serves as the receipt of, or as a substitute for, individualized investment advice from OSAM. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that any account holdings would correspond directly to any comparative indices. Account information has been compiled solely by OSAM, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this presentation, OSAM has relied upon information provided by the account custodian and/or other third party service providers. OSAM is a Registered Investment Adviser with the SEC and a copy of our current written disclosure statement discussing our advisory services and fees remains available for your review upon request.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

Notes: All factor portfolios cited in this are calculated using a compositing methodology. Monthly portfolios are created with a 12-month holding period based on a single characteristic within a universe of stocks. The 12 monthly portfolios are then combined together to create the composite portfolio.

Universes: The All Stocks Universe includes all stock included in the Compustat Database listed on a U.S. exchange with a market value greater than $200mm and a price per share greater than $1. The Worldscope Universe consists of over 25,000 currently active companies (and 7,000 inactive companies) in developed and emerging markets (across over 50 countries in total), representing approximately 97% of global market capitalization.

The dividend yield is a gross indicated yield. There is no guarantee that the rate of dividend payment will continue and the income derived is subject to taxes and expenses which will impact the actual yield experience of each investor.