Price-to-Book’s Growing Blind Spot

By Chris MeredithNovember 2016

Value has broadly been accepted as an investing style and, historically, portfolios formed on cheap valuations have outperformed expensive portfolios. But value comes in many flavors, and the factor(s) you choose to measure cheapness can determine your long-term success. In particular, several operating metrics of value, such as earnings and EBITDA, have outperformed the more traditional price-to-book (P/B) factor. A possible reason for the limited efficacy of price-to-book is because of the increase in shareholder transactions, primarily through the increase in share repurchases.

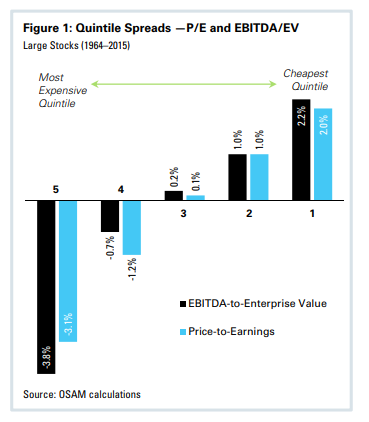

Valuation factors have the benefit of being simple, but can also have flaws. Price-to-sales has the benefit of measuring against revenue, which is difficult to manipulate, but it doesn’t take margins into account. Price-to-earnings (P/E) measures against the estimated economic output of the company, but also contains estimated expenses that can be manipulated by managers. EBITDA-to-enterprise-value (EBITDA/EV) has the benefit of including operating cost structures, but it misses payments to bondholders and the government. Even with these flaws, the factors are effective in practice. Figure 1 shows the quintile spreads of two factors within a universe of U.S. Large Stocks from 1964 through 2015

Price-to-book is perhaps the most widely used valuation factor in the investing industry. Russell, the top provider of style indexes for the U.S. market, uses the factor as its primary metric to separate stocks into Value and Growth categories. They use price-to-book in combination with forecasted two-year growth and historical five-year sales-per-share growth, but price-to-book is the chief determinant, comprising 50 percent of the methodology. Russell’s choice of price-to-book most likely comes from its long history in academic research. The seminal work on price-to-book is Fama-French’s 1992 paper “The Cross-Section of Expected Stock Returns”, which established the three-factor model of Market, Size, and Price-to-Book.

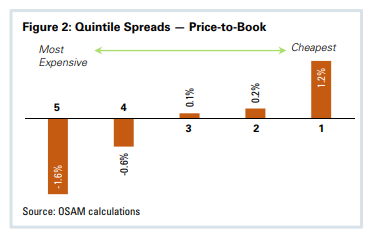

But when you start looking closely at price-to-book, a few issues start to become apparent. First, the overall spread on the factor isn’t as strong as it is with other operating metrics. The spread between price-to-book’s highest and lowest quintiles (see Figure 2) is only 2.8 percent—versus price-to-earnings’ 5.1 percent spread and EBITDA-to-enterprise value’s 6.0 percent spread.

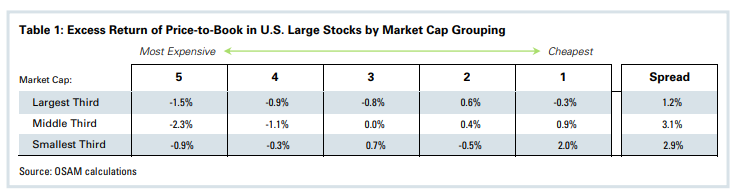

Second, when breaking down the efficacy of the factor based on market capitalization, price-to-book is least effective within the largest cap stocks. Table 1 shows the same quintile spreads of price-to-book in the U.S. Large Stocks universe, but separates out the smallest and largest third based on market cap. Price-to-book degrades in efficacy as the market cap gets larger—the quintile spread within the largest third of stocks is only 1.2 percent. This is especially noteworthy because Russell market cap-weights their benchmark and about two-thirds of it is in that Largest Third (with the lowest price-to-book spread of the three Large Stocks groups).

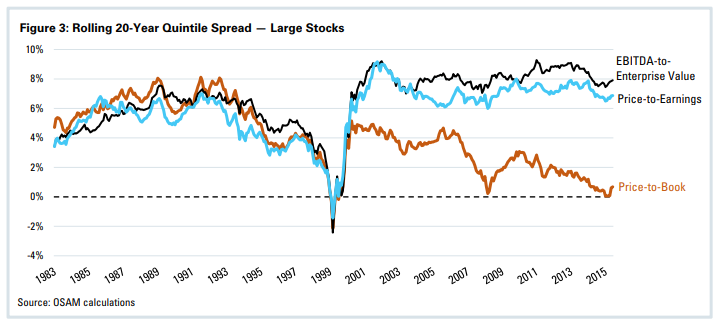

Last, the efficacy of price-to-book has been waning, especially since the turn of the century. Figure 3 shows the rolling 20-year quintile spread (the difference between the portfolio of the cheapest 20 percent and the portfolio of most expensive 20 percent). Comparing price-to-book against EBITDA-to-enterprise value and price-to-earnings, it shows how all three metrics behaved very similarly before 2000. They had generated consistent outperformance until being inverted in the dot-com bubble of the late 1990s, when the most expensive stocks outperformed. But coming out of the dot-com bubble, price-to-book has started behaving differently than other valuation factors, degrading to the point where for the past 20 years it has had almost no discernible benefit on stock selection.

On the surface, using book value in relation to price makes intuitive sense. The book value of equity is the total amount of common equity shareholders would receive in liquidation (the difference between the accounting value of the total assets and the total liabilities and preferred equity). The price-to-book factor is meant to be a quick measure for seeing how cheaply the company could be acquired. The factor will move around based on changes in either the market value or book value of equity. But the factor comes with assumptions. “Clean surplus accounting” is based on the assumption that equity only increases (or decreases) from the earnings (or losses) in excess of dividends. In practice, there is another influence on equity: transactions with shareholders.

When a company repurchases shares, the market effect is straightforward. The number of shares outstanding are reduced while the price remains the same, so the market capitalization goes down. When taking the share buybacks into account for financial reporting, the repurchase of shares does not create an asset as if the company had repurchased equity in another company. Instead, the equity value is decreased by the amount spent in purchasing the shares.

As a hypothetical example, take a company with a $200 million market cap, $100 million in book value of equity, and $10 million in earnings. The company has a price-to-earnings ratio of 20, and a price-to-book ratio of 2.

If that company becomes an aggressive Repurchaser and decides to acquire $50 million worth of its own equity, it will alter the results significantly. The earnings remain the same but the market cap goes down, adjusting the priceto-earnings down to 15. But the price-to-book ratio will be reduced on both the top and bottom and it will actually increase to three.

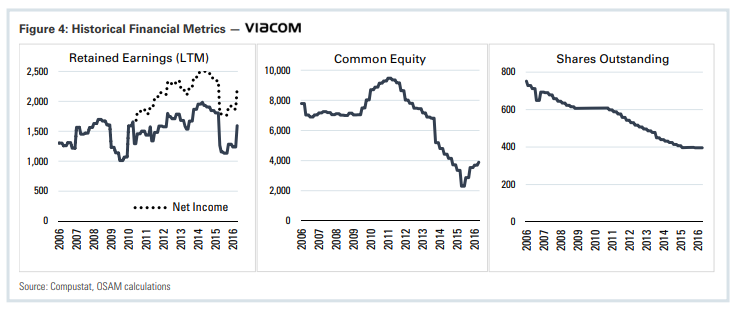

As a practical example, Viacom has been aggressively repurchasing its own shares after separating from CBS in 2006, spending almost $20 billion over the past ten years. In 2015 alone, it repurchased about $1.4 billion in shares. So even though the company has been seeing retained earnings of about $1.5 billion per year, its common equity has reduced from $8 billion to $4 billion over that same time frame.

You can see how this distorts valuation factors. Viacom trades at a significant discount on earnings versus the median price-to-earnings for other large stocks, while at the same time looking as though it trades at a significant premium on the book value of equity.

A company issuing shares will have the reverse effect. The company will actually increase its book value, even though the earnings and cash flows are diluted across more investors. Any transaction for a company, through the issuance or reduction of equity, flows through the book value of the equity.

Table 2 compares median valuation factors for companies with a market capitalization greater than average. Two groups are compared with the median large stock: those companies that have repurchased the most shares over the past five years (Repurchasers) and those that have issued the most shares (Diluters). The top 25 Repurchasers have better operating valuation metrics (e.g., sales, earnings, EBITDA, free cash flow) than the median, and the top 25 Diluters have worse results—with the standout exception of price-to-book. Repurchasers have an average price-to-book of 4.5, almost 20-percent higher than the median 3.8, while Diluters look cheap with a price-to-book of only 2.7—an apparent discount of almost 30 percent.

This distortion suggests that using price-to-book could lead to misclassifications of stocks as a Value investment. Stocks that are cheap on operating metrics like sales, EBITDA, or earnings could end up classified as Growth. Conversely, that universe could include a company that has issued a lot of stock and has inflated its book value of equity. This is something to keep in mind, as a number of quantitative managers start with the benchmark as their universe. Starting with the Russell 1000® Value could bias you towards a number of companies that look cheap on price-to-book but are not cheap on other important valuation metrics.

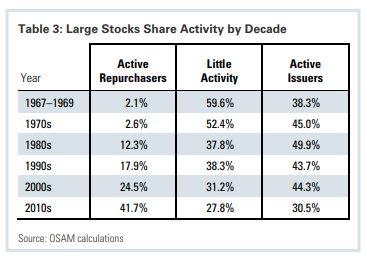

Over the past fifty years, there has been a gradual increase in the amount of company equity transactions. In particular, larger companies have been increasing their share repurchase activity. In classifying companies based on a trailing five-year change in shares outstanding, we can see which companies have consolidated shares by more than five percent, issued shares more than five percent, or have been relatively inactive. In 1982, the U.S. loosened regulation around a company’s restrictions for repurchasing shares and there has been a significant increase in activity. This has led to a change in the overall market, where the percentage of companies inactive has been reduced—from almost 60 percent in the 1960s down to around 28 percent—with the activity mainly being driven from companies consolidating shares.

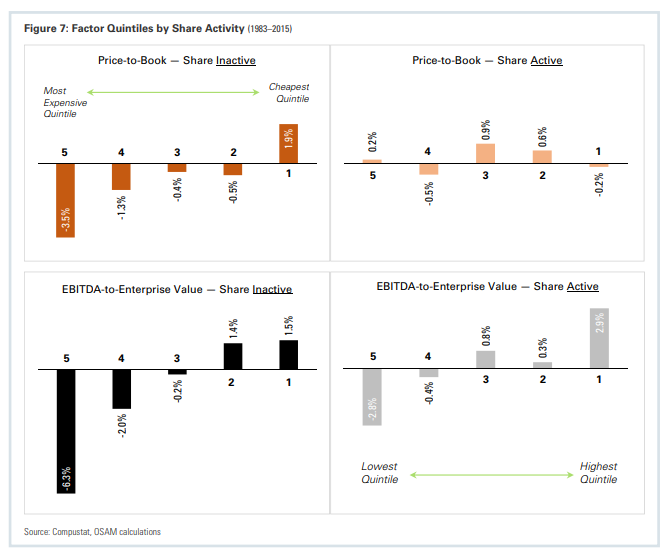

This begs the question: Does a moderate increase in shareholder transactions result in price-to-book gradually becoming ineffectual as a valuation factor? The first rule in analysis is not to confuse correlation with causation. However, the rolling 20-years when price-to-book has been less effective coincides quite well with the increase in shareholder transaction activity. Price-to-book is also the least effective in the largest cap stocks, which have the greatest volume of dollars affecting book value of equity. Perhaps the most interesting analysis is looking at the efficacy of price-to-book within those large stocks that have been relatively inactive with shareholders over a trailing five-year period versus those that have been active,

either on issuance or repurchase. From the 1982 legislation change to the present, there is a different level of valuation metrics’ efficacy for companies that are active or inactive with shareholders. If your investments are focused on companies with share issuance or repurchase activity, there has been no relative benefit to buying companies that look cheap on price-to-book and there’s almost no difference between high and low valuations. But, when limited to companies that are relatively inactive, you can get a spread of 6.4 percent between the highest and lowest 20 percent based on the price-to-book factor. Using a different valuation metric, such as EBITDA-to-enterprise value, works well—regardless of a company’s activity in issuing or repurchasing shares.

Even with the long-term degradation of returns from price-to-book, it is possible that it may revert to an effective investment factor. Price-to-book has been off to a strong start in 2016 and is outperforming other valuation factors, particularly in small cap stocks. But there are structural challenges to the factor and, before using it, investors need to be made aware of the embedded noise from repurchases that could be misleading.

General Legal Disclosures & Hypothetical and/or Backtested Results Disclaimer

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

The risk-free rate used in the calculation of Sortino, Sharpe, and Treynor ratios is 5%, consistently applied across time.

The universe of All Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than $200 million as of most recent year-end. The universe of Large Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than the universe average as of most recent year-end. The stocks are equally weighted and generally rebalanced annually. Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight. The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.