Emerging Markets – The Growing Opportunity

By Claire NoelJuly 2021

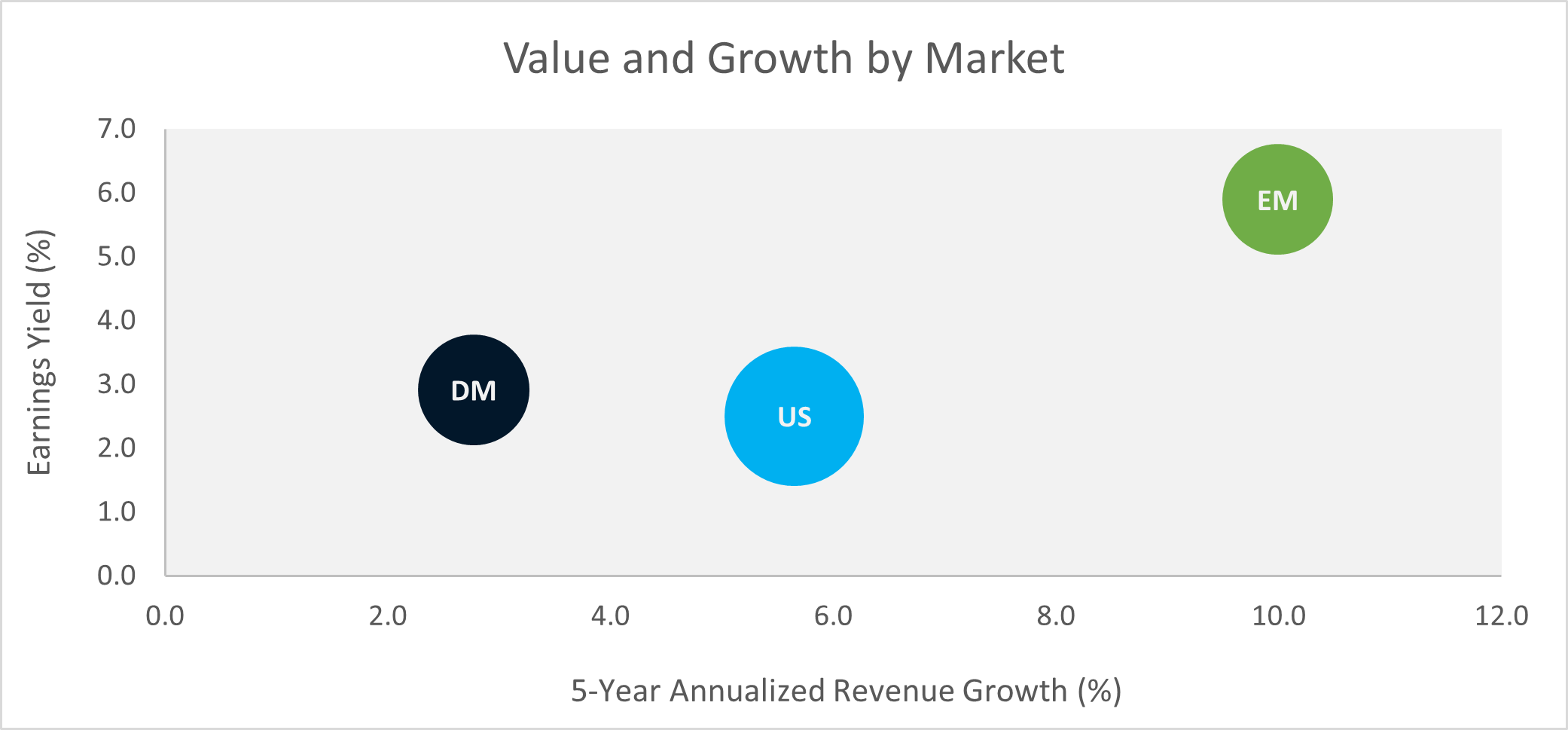

Figure 1: Value and growth for emerging markets (EM), developed markets ex-U.S. (DM), and the United States (U.S.). Earnings yield is computed as sum(trailing 12-month earnings)/sum(market capitalization) as of 6/30/2021. Revenue growth is a compound annual growth rate (CAGR) from 12/31/2015 through 6/30/2021 with dividends converted into share buybacks. Both measures are computed over a universe of the largest 12,000 companies world-wide. Bubble size corresponds to the relative market cap in each region.

Introduction

This week we launched a suite of international emerging markets (EM) and developed markets (DM) ADR strategies on Canvas.

We believe there is a compelling case for investing overseas, specifically in emerging markets due to their increasing accessibility, rapid growth, attractive valuations, and diversification potential. We discuss some highlights below.

Background

Historically, emerging markets have been difficult for the average U.S. investor to access. Low liquidity, high costs, mounds of paperwork, and foreign investor restrictions were, and still are, major impediments to direct investment.

Fortunately, some of those barriers have lifted. There are now more than 400 liquid American Depository Receipts (ADRs) representing companies located in emerging markets, as well as a broad array of emerging markets ETFs.

Growth and Value Opportunities

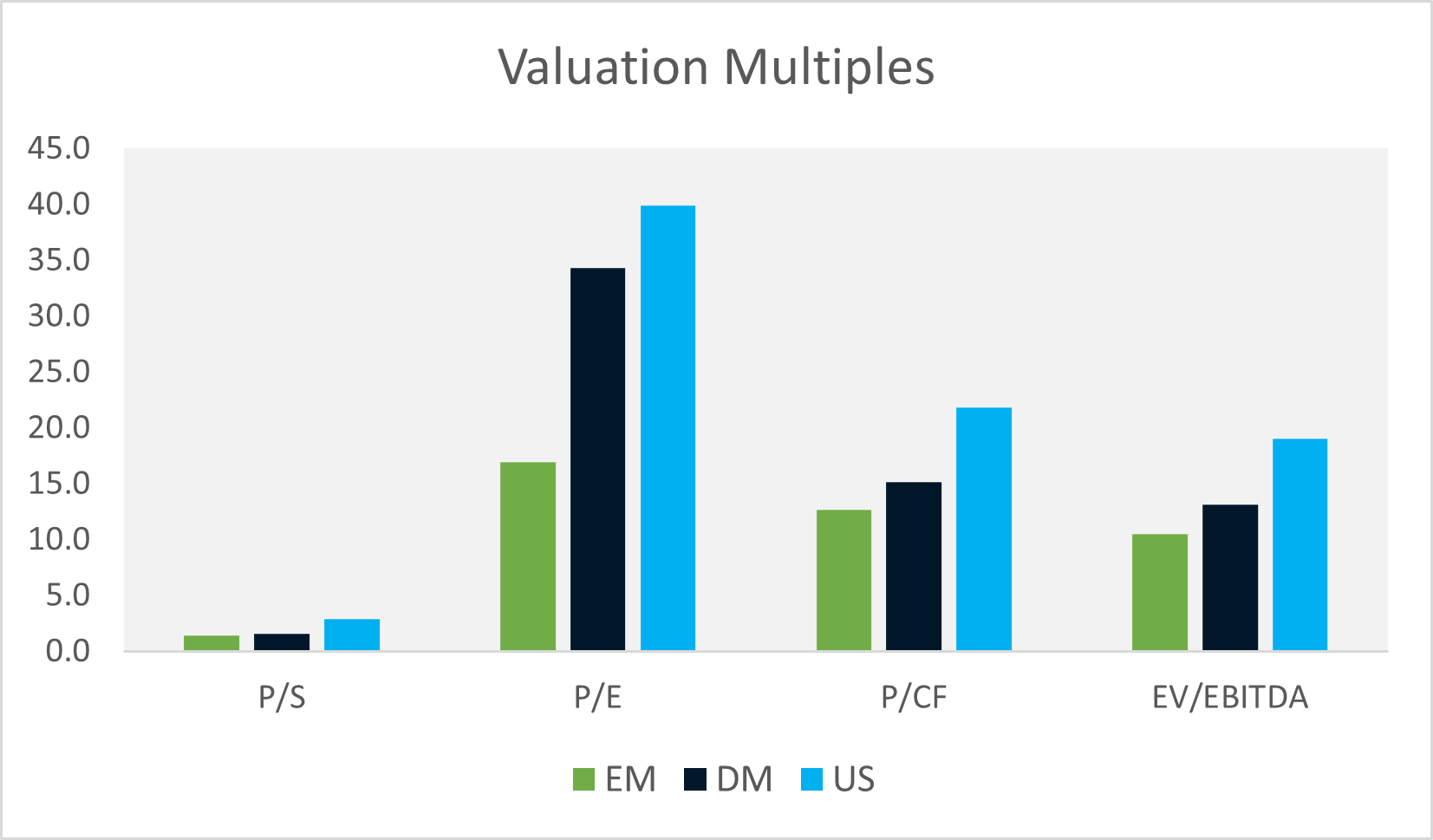

It is difficult to find high expected returns with equity prices at all-time peaks; however, on a relative basis, emerging markets look like a bargain with a P/E multiple of 17x versus 34x and 40x in developed international and the U.S. respectively.

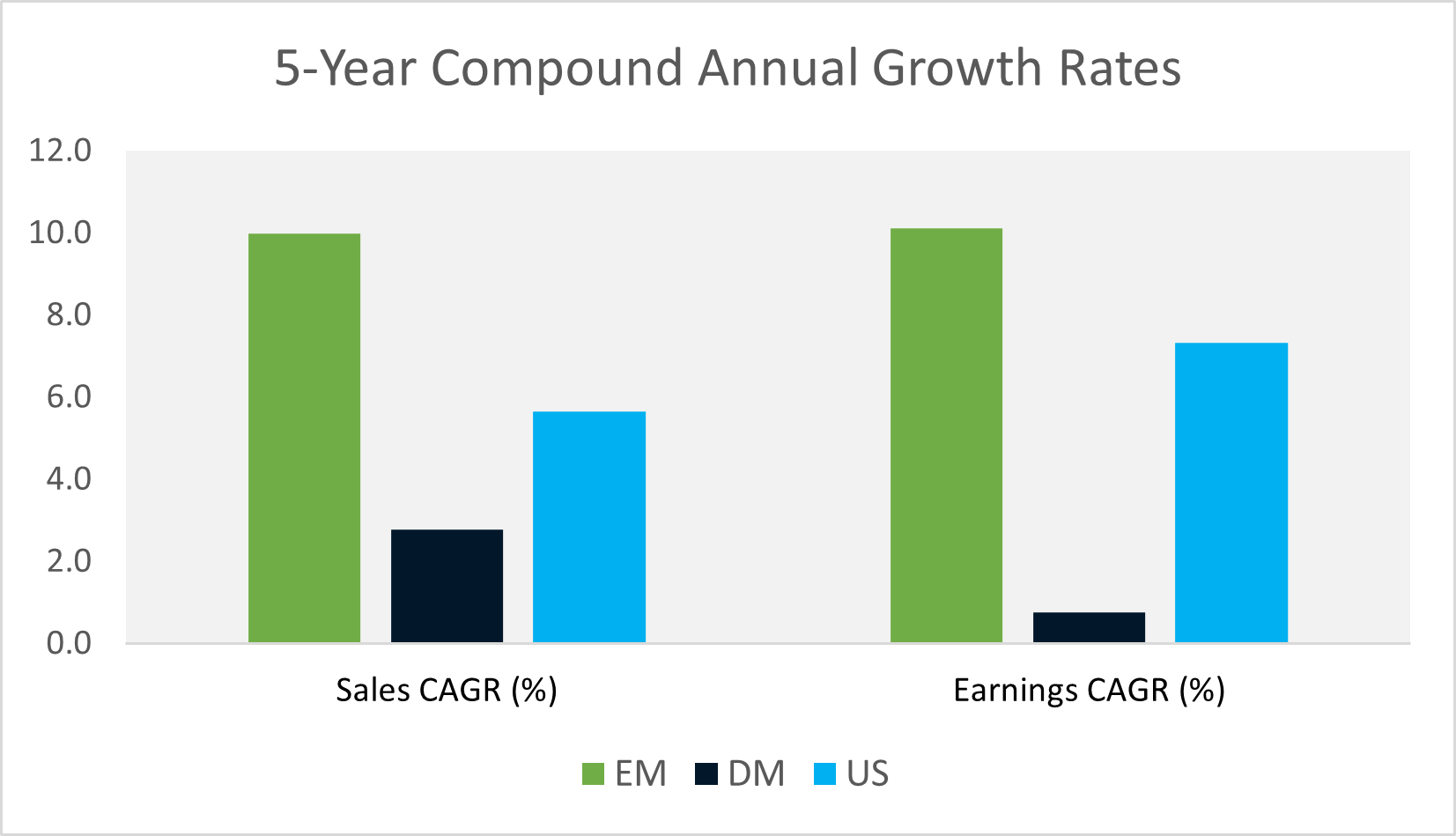

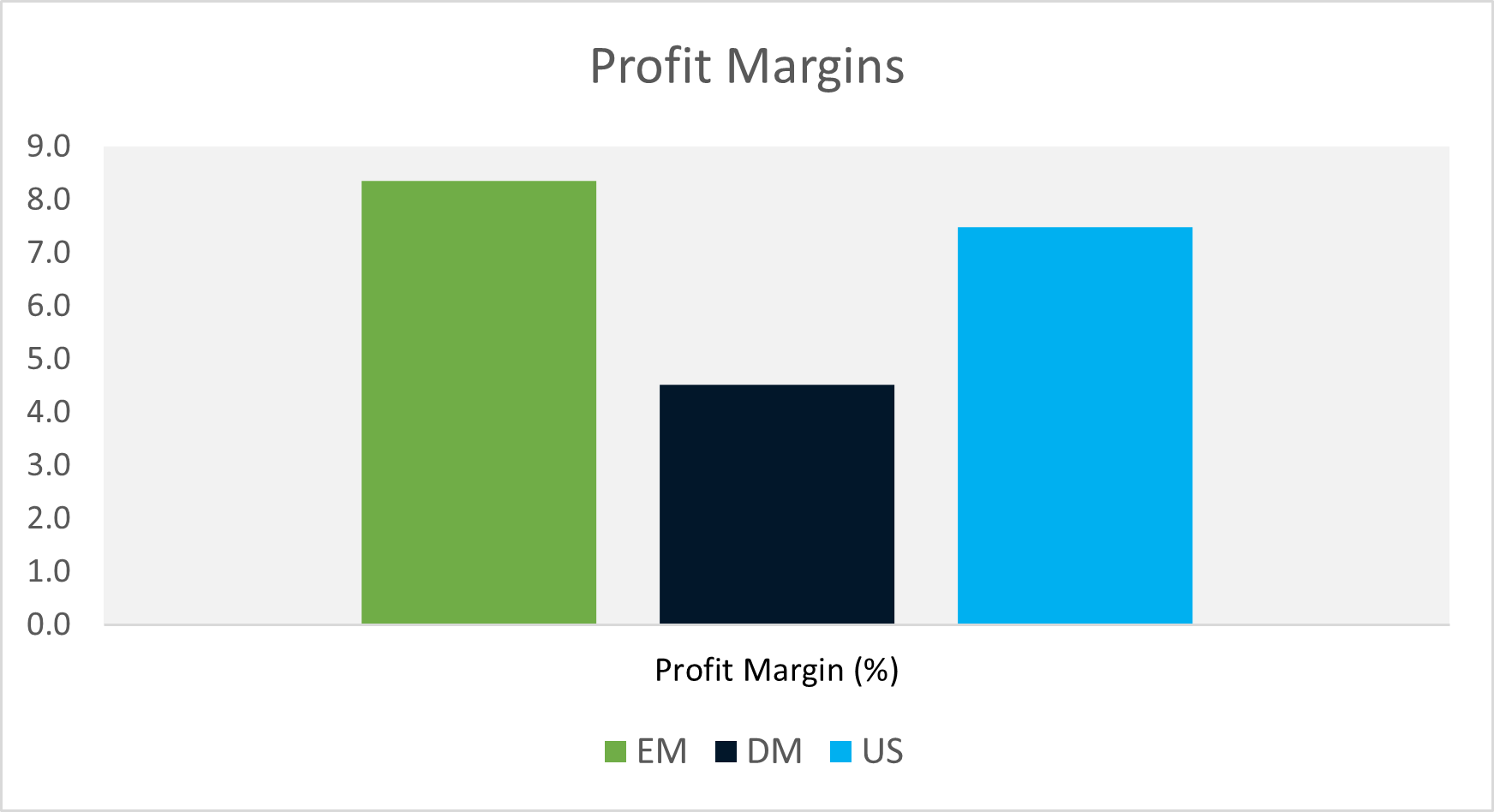

EM companies are not cheap for lack of fundamental earning power either. In fact, they have higher growth and profit margins than both the U.S. and developed international regions. Valuations may be suppressed for other reasons, such as policy and ESG concerns, but if (or when) they revert to long-term fundamentals, the returns could be lucrative.

Figure 2: Valuation multiples are computed as sum(market capitalization or enterprise value)/sum(trailing 12-month sales or earnings or cash flows or EBITDA) as of 6/30/2021. All measures are computed over a universe of the largest 12,000 companies world-wide.

Figure 3: Growth statistics are compound annual growth rates (CAGR) from 12/31/2015 through 6/30/2021 with dividends converted into share buybacks. Both measures are computed over a universe of the largest 12,000 companies world-wide.

Figure 4: Profit margin is computed as sum(trailing 12-month net income)/sum(trailing 12-month sales) as of 6/30/2021 over a universe of the largest 12,000 companies world-wide.

Diversification

“I view diversification not only as a survival strategy but as an aggressive strategy, because the next windfall might come from a surprising place.” - Peter Bernstein

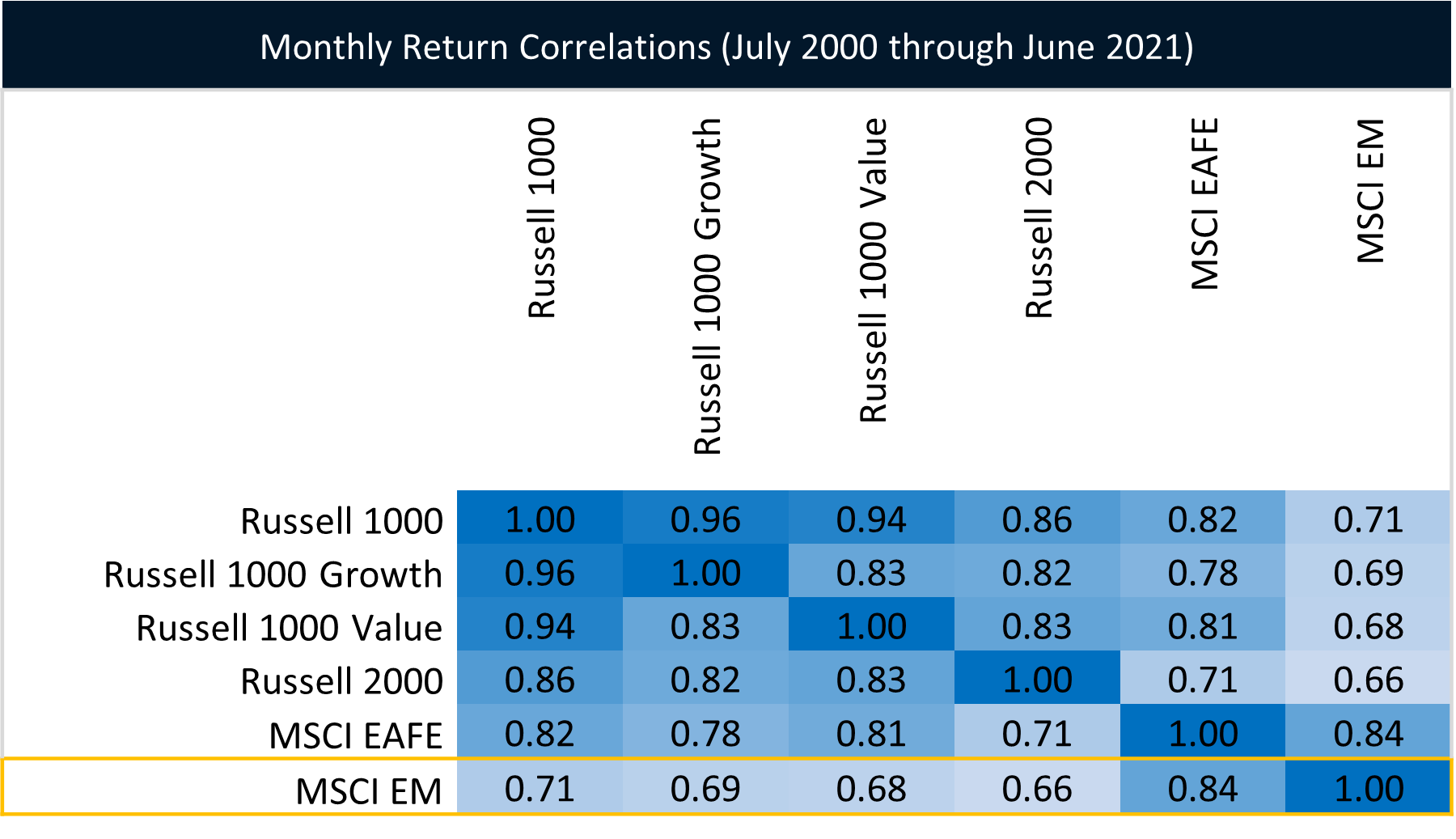

Another reason to consider allocating to emerging markets is their relatively low correlation with developed markets. Many investors think about diversifying along the dimensions of U.S. and international, value and growth, and large and small cap. The MSCI Emerging Markets index has some of the lowest correlations with each of those segments, making it an effective diversification play, even for investors choosing among index-replicating equity strategies. Below we show the monthly return correlations among several major indices, representing different market caps, styles, and geographic buckets. A lighter blue color corresponds to a weaker relationship between month-to-month returns.

By extension, active EM strategies have even more diversification potential, which leads us to opportunities in active management.

Figure 5: Spearman rank-order correlations of monthly index returns from July 2000 through 2021.

Opportunities for Active Management

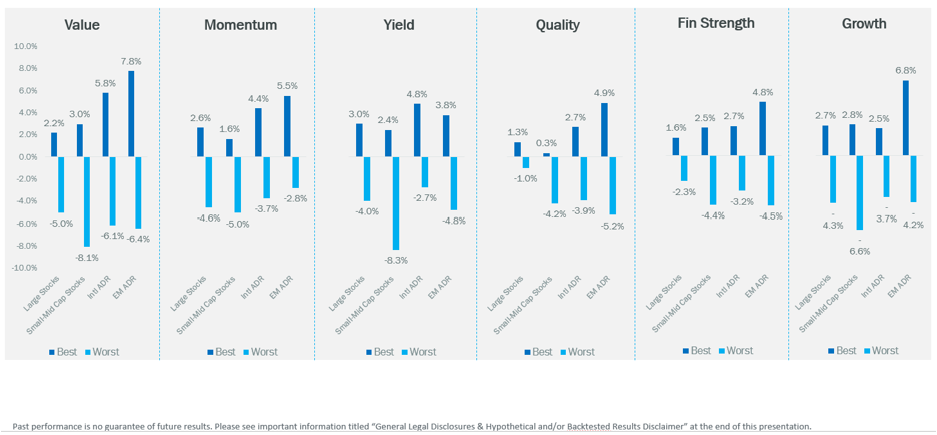

Emerging markets tend to be less efficient, and with that inefficiency comes greater opportunity for active managers to outperform. Decile return spreads to each of OSAM’s factors are almost uniformly wider in EM than in other regions of the world. The long-term returns to value and growth are particularly strong, creating ripe opportunities for active managers presently.

Figure 6: Benchmark-relative top and bottom decile returns within OSAM’s U.S. Large Cap, U.S. Small Cap, developed international ADR, and emerging markets ADR investment universes for the period spanning January 1996 through April 2021.

China – Too Big to Ignore

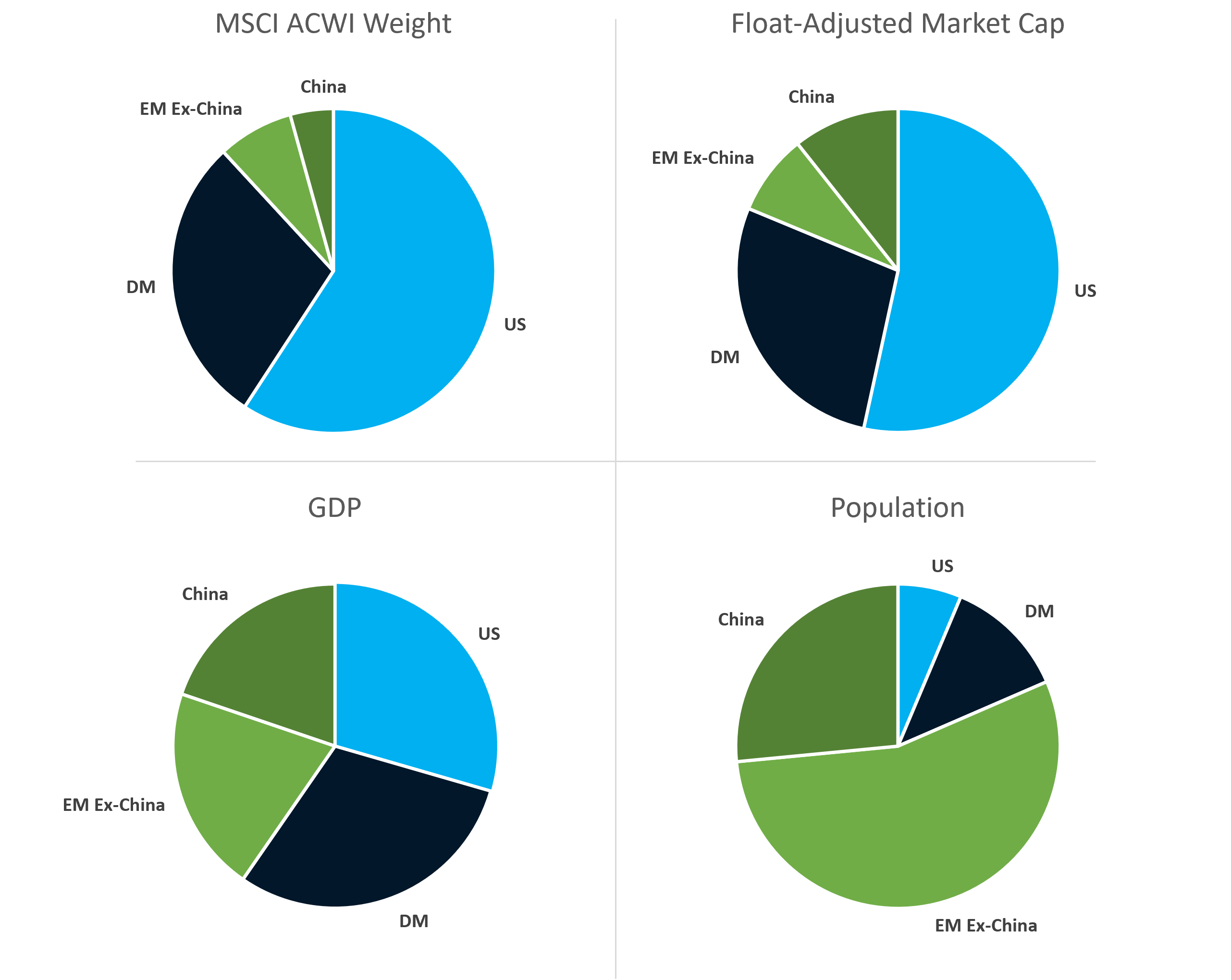

Finally, a discussion of emerging markets would be incomplete without mention of China. China is by far the largest country in the MSCI EM index with a weight of 37%. It is also the most populous country in the world and second only to the United States in terms of GDP. However, it is still exceedingly under-represented in most passive equity allocations with a weight of only 4.8% in the MSCI ACWI. China’s full float-adjusted market cap is closer to 10% of world markets and 50% of emerging markets. This is a big gap, by far the largest gap in country representation.

On the heels of the “China Connect”1 access program that allows foreigners to access local Chinese markets, index providers are beginning to recognize China’s influence in world markets with roadmaps for A-Shares2 inclusion and specialized China indices3.

Despite political tensions between the U.S. and China, at least 20 Chinese companies have already gone public in the U.S. this year, furthering the trend of improving market accessibility and demonstrating Chinese business owners’ strong desire for foreign funding.

In the near term, the mechanisms by which Chinese markets open to U.S. investment may largely depend on the U.S. and China’s foreign policies, but given the heft of both countries’ economies, it is almost inevitable that they will become ever-more integrated and important to investors. The increasing recognition of China’s weight in passive allocations, along with improvements in foreign access, could provide a strong structural tailwind for Chinese equities.

Figure 7: MSCI weights and float-adjusted market caps as of 6/30/2021. The break-down of float-adjusted market cap is based on a universe of the largest 12,000 companies world-wide. GDP and population are sourced from the World Bank (https://data.worldbank.org/indicator/NY.GDP.MKTP.CD and https://data.worldbank.org/indicator/SP.POP.TOTL).

Conclusion

We have outlined several reasons to invest in emerging markets, namely high expected returns and diversification; however, there is inherent risk. We believe that current prices reflect more risk than warranted, but it is risk, nonetheless. Canvas empowers investors to decide how to precisely allocate to developed, emerging, and U.S. markets while also managing for taxes and ESG preferences. Armed with a customizable toolset, we leave the decision to our partner clients and look forward to the feedback.

FOOTNOTES

1 https://www.hkex.com.hk/Mutual-Market/Stock-Connect?sc_lang=en

2 China A-shares trade on the two Chinese mainland stock exchanges, the Shanghai Stock Exchange (SSE) and the Shenzhen Stock Exchange (SZSE). Historically, only mainland citizens could own China A-shares due to restrictions on foreign investment. Now, via the China Connect mutual market access program, foreigners can invest in mainland companies.

3 https://www.msci.com/our-solutions/indexes/china-investing

https://www.ftserussell.com/index/spotlight/china-indexes

GENERAL LEGAL DISCLOSURES & HYPOTHETICAL AND/OR BACKTESTED RESULTS DISCLAIMER

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

The risk-free rate used in the calculation of Sortino, Sharpe, and Treynor ratios is 5%, consistently applied across time.

The universe of All Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than $200 million as of most recent year-end. The universe of Large Stocks consists of all securities in the Chicago Research in Security Prices (CRSP) dataset or S&P Compustat Database (or other, as noted) with inflation-adjusted market capitalization greater than the universe average as of most recent year-end. The stocks are equally weighted and generally rebalanced annually.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

- Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

- OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

- OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

- The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

- The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

- The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

- Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

- Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

Please Note: Socially Responsible Investing Limitations. Socially Responsible Investing involves the incorporation of Environmental, Social and Governance considerations into the investment due diligence process (“ESG). There are potential limitations associated with allocating a portion of an investment portfolio in ESG securities (i.e., securities that have a mandate to avoid, when possible, investments in such products as alcohol, tobacco, firearms, oil drilling, gambling, etc.). The number of these securities may be limited when compared to those that do not maintain such a mandate. ESG securities could underperform broad market indices. Investors must accept these limitations, including potential for underperformance. Correspondingly, the number of ESG mutual funds and exchange traded funds are few when compared to those that do not maintain such a mandate. As with any type of investment (including any investment and/or investment strategies recommended and/or undertaken by OSAM), there can be no assurance that investment in ESG securities or funds will be profitable, or prove successful.