Value Is Dead, Long Live Value

By Chris MeredithJuly 2019

EXECUTIVE SUMMARY

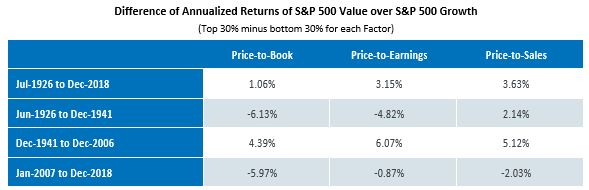

- Value has underperformed since the beginning of 2007. Another prolonged period of underperformance for Price-to-Book and Price-to-Earnings happened between 1926 and 1941.

- This paper offers a theory for the connection between the two periods: they coincide with the central turning point of Technological Revolutions. There have been five revolutions identified: clusters of innovation that replace existing business models through creative destruction.

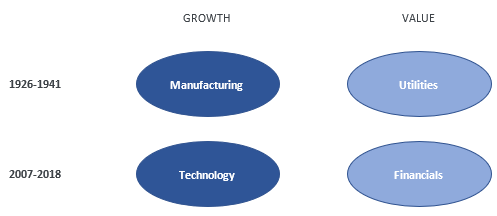

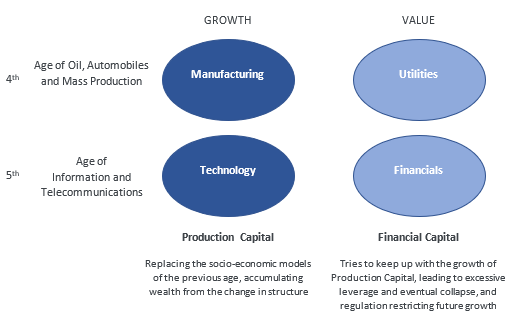

- The fourth revolution was the Age of Oil, Automobiles, and Mass Production, where manufacturing of cars and their components (Oil, Steel, Rubber) flourished. Conversely, Railroads and Utilities, the infrastructure from the third revolution, declined amidst lower demand, a financial crisis and increased regulation.

- The fifth revolution is Information Technology, where the internet and mobile computing take hold while Financials declined amidst a financial crisis followed by heightened regulation.

- In both periods, collapses of financial capital in Utilities (1926-1941) and Financials (2007-2018) had significant impact on the Value portfolios.

- Technological Revolutions come in long waves, but eventually stabilize in deployment of new socioeconomic norms. Value investing has historically outperformed after we transition from the turning point.

Introduction

Value investing is a bedrock principle for quantitative and fundamental equity managers, as there is long-term efficacy to buying cheap stocks over expensive growth stocks. While Value investing remains attractive over the entire history of available data, it has been under extraordinary pressure since the beginning of 2007. As of June 30, 2019, the Russell 1000 Value has underperformed the Russell 1000 Growth by a cumulative -136%, for an annualized return gap of -4.3% over twelve and a half years. Since the middle of 2017 alone, Value has trailed an additional -21%. This recent underperformance has left the investment community on its heels, as Value managers struggle to explain why their style has been out of favor for so long, and allocators question overweight positions in Value.

The severity and length of Value’s underperformance will entice some to capitulation. This may take the form of terminating a manager with a sound investment process, and proven track record, or adjustments to strategic allocations because “Value is dead”.

At OSAM, we believe that the key principle to investment success is maintaining one’s discipline in periods when performance works against you. Discipline is fostered from a conviction in the investment process. And conviction is born out of extensive research. This research piece attempts to answer the questions about Value’s underperformance by setting this most recent period within a larger historical context, providing some explanations for why we are in a Growth Regime, and try to set expectations for if, and when, Value investing will return to favor.

Growth Regime(s)

The main question investors face is whether this underperformance is structural or episodic; is Value investing broken forever or simply in an extended bad run. Part of the challenge in answering this question is that most investment research does not include any periods of Value underperformance lasting over twelve years, leading investors to believe that it’s different this time.

In our search for perspective, we extended the research to include new time frames. Most research starts in 1963 because that’s when Compustat, the main data provider for historical financial statements, has quarterly availability for income statements. There is also a data set collected by Ken French providing the Book Value of Equity back to 1926, which does allow for some extended research. At OSAM, we like to utilize multiple valuation metrics in our research. To try and gain new insights into whether this Regime of Growth is structural or episodic, OSAM created a new set of fundamentals, which we call Deep History, that extends revenue and earnings data for individual companies back to June-19261. The combination of these datasets with the CRSP pricing database allows us to conduct ninety-two years of historical research on Value Investing for three ratios: Price-to-Book, Price-to-Earnings and Price-to-Sales. In order to ensure that we are working with investible and replicable universes, we also utilize the S&P 500 constituents available through CRSP to create Value and Growth portfolios. For specifics on Data and Methodology, see appendices A & B.

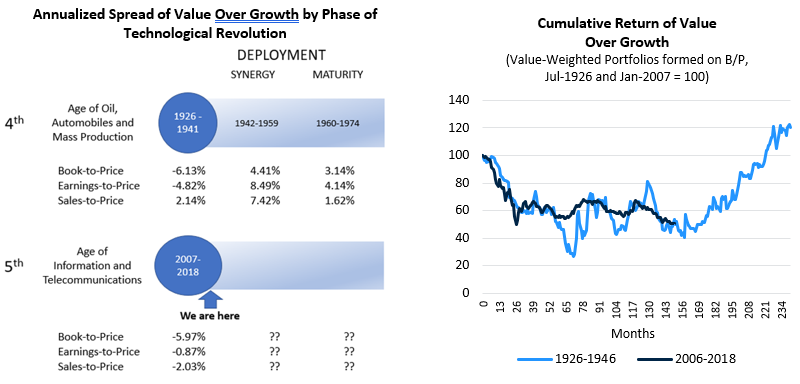

The broad conclusion is that across the entire 92-year time frame, Value investing has been an effective investment strategy generating higher returns than Growth stocks. But by including the earliest time frame back to 1926, we discovered another period where Value investing struggled as badly as it has today: a second Growth Regime from July of 1926 through 1941.

Attribution (see Appendix C) on these time frames shows there were specific sectors2 in Value and Growth that had significant contributions to the return of the portfolio. For the Growth portfolios, Manufacturing stocks from 1926-1941 were primarily in the Growth portfolio, as were Technology stocks from 2007-2018. For the Value portfolios, Utilities3 were primarily in the Value portfolio for the earliest Growth regime, while Financials were clustered in Value in the most recent portfolio.

Technological Revolutions

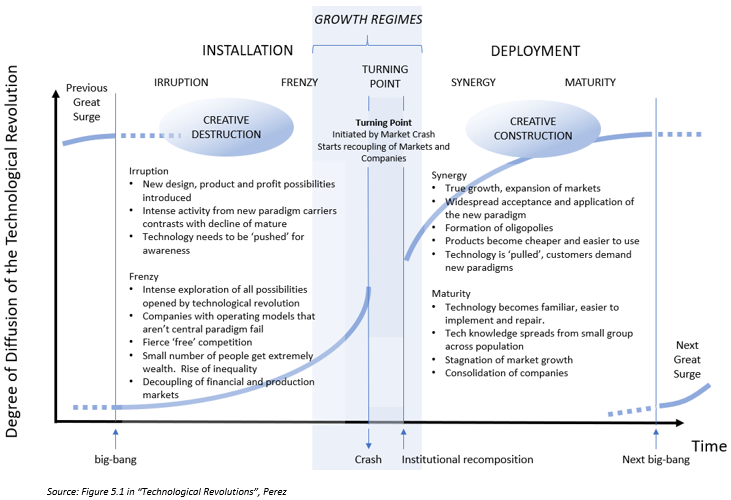

The history of these two periods is complex and difficult to summarize, but economic models are useful for simplifying large scale trends into something digestible and applying one may provide insights. With both Growth regimes lasting twelve to fifteen years, but sixty-seven years apart, they are best studied through the lens of the long-term economic cycle of Technological Revolutions4.

Technological Revolutions are clusters of new technologies that cause economic upheaval over periods lasting 45 to 60 years. The cycles start with the discovery of ideas, an installation of infrastructure to make it scalable, followed by a deployment with strong growth that eventually results in maturity, where growth slows down. In her work “Technological Revolutions and Financial Capital” (2002), Carlota Perez identifies the phases of a revolution as two halves: the Installation phase and Deployment phase.

In the Installation phase of a new Technological Revolution, the previous revolution is nearing exhaustion of profitable opportunities. Then, through experimentation new social and economic norms are established for the utilization of ideas. As these concepts take shape and the form factor for utilization is established, people see the potential growth and infrastructure is laid for their widespread adoption. This Installation phase is one of creative destruction, as the new standards replace those from preceding revolutions. It is a period where wealth becomes skewed as innovators are rewarded.

As the new technology shifts to becoming the new norm, the Deployment phase begins. It takes advantage of the infrastructure laid in the Installation phase and expands to broad societal acceptance. This begins with a high growth phase, where real growth occurs, and the technological revolution diffuses across the whole economy. Entrepreneurial activity moves from building infrastructure to the application layer on top. This is a time of creative construction. Winners emerge to form oligopolies, and this growth eventually slows to the Maturity phase, where market growth stagnates.

This framework has played out several times in history, with technologies like the light bulb. Experimentation occurred over decades with electric arc lamps and vacuum tubes, until Thomas Edison perfected the carbonized filament bulb in 1880, setting the form factor for electric lighting. The coincident innovations of power generation and electrical infrastructure were also required, but after the Installation of the paradigm, there was a rush of applications for it: longer business shifts, the first night-time baseball game. Once the applications were discovered, it was simply a matter of Deployment to electrify the country and change how we lived. Eventually the ideas reach maturity and commoditization, and now dozens of light bulbs are in every house.

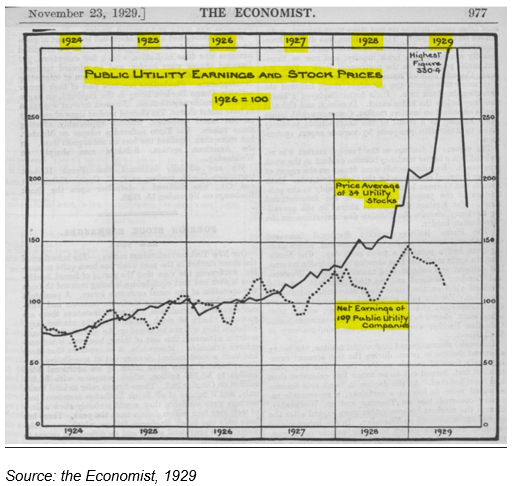

Timing when these revolutions start and end is subject to interpretation, but Perez’s model incorporates some specific timing for phases through a couple of key observations. The first is a “big-bang” event of technological innovation, highly observable events of technological progress. The second timing signal are market bubbles that naturally occur from a technological revolution. Perez makes a distinction between production capital and financial capital: “Financial Capital represents the criteria and behavior of those agents who possess wealth in the form of money or other paper assets. Production Capital embodies the motives and behaviors of those agents who generate new wealth by producing goods or performing services.“5 As the norms begin to scale, a “Frenzy” begins where financial capital outstrips production capital, producing valuation bubbles. These bubbles indicate the beginning of the Turning Point. Financial capital eventually relinks, reestablishing normal valuations of the real production of companies, but this can take several years. There are significant failures during this period, as the winners are established.

Between the big bang initiations and the market bubbles, Perez can assign approximate time frames for phases of technological revolutions. She has identified five main technological revolutions, starting with the Industrial Revolution. The two most recent are the Age of Oil, Automobiles and Mass Production (1908-1974) and the Age of Information and Telecommunications (1971-present).

In her model, the two Growth Regimes we have identified are right in the middle of the turning points for the 4th and 5th Technological Revolutions.

Source: combination of Table 2.3 and Figure 5.2 in “Technological Revolutions”, with an adaptation of the 5th turning point from Perez’s blog post at http://beyondthetechrevolution.com/blog/second-machine-age-or-fifth-technological-revolution-part-2/

The Age of Oil, Automobiles and Mass Production

Understanding how the innovation from a Technology Revolution changes societal behavior is central to comprehending how a Technological Revolution might affect Value investing. Any survey of a technological revolution in this piece will be superficial, but to gain perspective on what these phases look like, it’s informative to review what we know from the two previous revolutions.

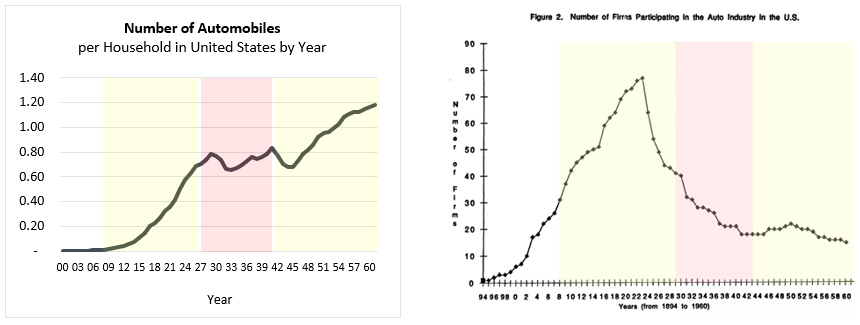

The key innovation from the 4th Technological Revolution was the convergence of internal combustion engines and cheap energy through gasoline to create the automobile. The production of automobiles started through craftsmen in the 1880s, where one commissioned a car to be custom made. At the time, the industry was trying several configurations to determine the best model for widespread adoption. At the turn of the century, in fact, steam and electric vehicles accounted for about three-quarters of the estimated four-thousand automobiles produced by 57 American firms6.

The big-bang in the automobile industry was Henry Ford’s new Highland Park Plant in Detroit. This plant set the manufacturing standards for automobiles by introducing the moving assembly line, where the body of cars were constructed while being transported along a moving platform. As the process evolved, Ford was eventually producing a car every two minutes. This innovation produced a host of organizational, managerial, social and technological changes resulting in the advent of mass manufacturing.

The automobile’s rise, however, was only possible because of the ubiquitous, cheap power from gasoline. Established in 1913 after Standard Oil developed the thermal cracking process through experimenting with the refinement of crude oil at various temperatures and pressures, oil became a core input to the rise of automobiles. The creation of an assembly line for mass production, and the commoditization of energy through gasoline are hallmarks of the Irruption phase.

The ensuing frenzy phase began with mass adoption of the automobile, which was fueled by Henry Ford’s focus on selling automobiles at low prices. Ford’s Model T was introduced in 1908 at $850 and was $360 by 1916, undercutting more expensive options like the electric car which cost $2,800 in 19137. Additionally, General Motors invented GMAC in 1919 to provide financing to auto purchasers, which solidified GM as the industry leader. Lower prices and access to capital resulted in mass adoption of the automobile and established the form factor still in existence today: gas powered internal combustion engine, a gear box, four wheels, control through pedals and a steering wheel. By 1929, the number of automobiles had risen to 0.80 per U.S. household8. With Chrysler, these rounded out the “Big Three” that would dominate automobile manufacturing for years to come, and it should come as no surprise that General Motors is the Growth portfolio’s top contributor from 1926 to 19419.

Growth wasn’t limited to just one product. Change was widespread as several other industries grew in tandem. These came directly from the inputs for manufacturing cars, but also indirect socioeconomic changes stemming from the automobile’s introduction. Focusing on the direct raw inputs for cars, by 1929, automobile production consumed 73% of the plate glass, 60% of strip steel, and 84% of the rubber, 52% of the malleable iron, and 37% of the aluminum produced in the United States, as well as significant amounts of copper, tin, lead, and nickel10. Consequently, companies producing those basic materials all experienced significant growth.

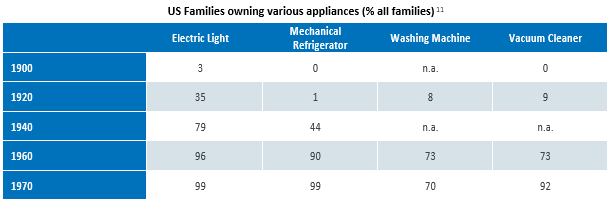

As the Technological revolution moved to Deployment, the scope of the social after-effects from the automobile and mass manufacturing is so wide that it is difficult to capture. For example, the application of organizational and managerial strategies from the moving assembly line created other industries like home appliances. This was possible because of transportation infrastructure from trucking and the ability for shipment of goods to the household. These appliances changed everyday life; with the average number of hours each household spends on housework plummeting from 58 hours a week in 1900 to 18 hours by 1975.

In the same vein, the automobile altered how people shopped. Previously, the consumer experience had been limited to goods provided by local craftsmen and mail order catalogs. Everything changed in 1924 when Robert E. Wood joined Sears, Roebuck and Co. While Sears had only operated as a mail-order catalog business, Wood recognized that people in outlying areas would have greater access to urban retail areas because of the automobile. Sears created the first retail store in Chicago in 1925, and by 1929 the company had 300 locations. In 1931 retail sales topped mail-order catalogs for the first time and continued to grow. By the “middle of the twentieth century Sears’ domestic annual revenue was about 1% of U.S. GDP, equivalent of $180bn. (In 2016, Amazon’s… North American revenue was ‘only’ $80bn)”12. Sears’ primary and most successful innovation was its consolidated stores of mass-produced goods. The company knew that customers across a wide geographic radius could reach its locations, establishing the standard for American consumerism.

The Turning Point of 1926-1941

Think of the Installation phase as the long process of establishing the technologies that make a car work, as well as the process of building and financing them at a price point for mass consumption, and the Deployment phase as the refinement and mass adoption and maturation of the industry. The “Turning Points” is between these two phases, where the growth is the highest because the trend is just beginning, and the eventual winners from the industry are established. This is when Value underperformed Growth for a prolonged period.

Attribution for the Value and Growth portfolios helps quantify this shift. First, we can see a stark difference in sector allocations. 65% of the Growth portfolio is in Manufacturing stocks, contrasted to only 19% of the Value portfolio. Additionally, 74% of the Value portfolio was in Utilities, while the Growth portfolio only had a 12% allocation to this sector. Taken together, these add up to a little over half of the reason why Growth outperformed Value from 1926-194113.

Looking at individual stocks, we mentioned that General Motors is Growth portfolio’s top contributor, but other Manufacturers (e.g. General Electric, Eastman Kodak) and retailers (e.g. Sears, Woolworth) are large contributors as well. For the Value portfolio, Utilities and Railroads were the main detractors, as the railroads faced multiple headwinds: declining infrastructure from nationalization back in 1917-1920, and a structural competitive disadvantage from the comparative cost to run steam locomotives versus trucking. Oil also helped the Growth portfolio, as Standard Oil of NJ and Standard Oil of California (i.e. Exxon and Chevron) were top contributors. The rise of mass food production through National Biscuit, Standard Brands and General Foods also helped the Growth portfolio. ‘Old’ productions of the capital world like Coal, Iron, Steel, Shipbuilding and Cotton had flat to decreased demand from 1905 to 1936, while ‘new’ industries like Gasoline, Aluminum, Nitrogen and Artificial Silk tripled in size or more, generating strong growth for companies like Union Carbide & Carbon (now a part of Dow Chemical) and Allied Chemical & Dye (AlliedSignal became Honeywell).

The Age Information and Telecommunications

The similarity between these two ages, and of Manufacturing and Technology, is the broad societal changes introduced through innovation. The technology revolution started with the microprocessor back in 1971, but a steady pace of development has led to convergence for mass utilization over roughly the last fifty years. A popular statistic people quote to scale the advances in processing power is that the iPhone 6 can perform instructions 120 million times faster than the computers that landed Apollo on the moon. It’s akin to comparing the Wright brothers’ first plane in 1903 to a World War II “flying fortress” bomber. The areal density of disk space doubled every 13 months driving down the price of storage for digital content. Microsoft was founded in 1975, creating an operating system to develop software for productivity and entertainment. In 1977, Apple, Tandy and Commodore bundled these together to offer desktop computing at affordable price points for individual households. Like the Model T, having a price point that was affordable for individual households led to mass adoption. Routers and networking protocols started in the 1980s, followed by HTTP and HTML protocols for standardized development on top of them, which led to the explosion of internet services in the late 1990s.

Amazon was the early winner from the internet boom, as the leader in eCommerce. They created the business template, establishing trust so people would enter their credit card into a site. Comparing the fourth revolution to the fifth, Sears and retailers of the 1930s disrupted the craftsman market because the automobile allowed people to travel to department stores where they could shop for anything. Amazon partially unwound the retail model of the fourth age by offering a retail experience where you order online, and the goods are shipped to you. Some retail models (i.e. groceries) are still being established in the eCommerce age, indicated by Amazon purchasing Whole Foods.

Broadband changed the internet experience, as people migrated from dial-up connections over telephone lines to cable modems, allowing for richer media and higher interaction with sites. 3G wireless networks were introduced in 1998, followed by 4G in 2008, extending cellular service beyond voice and messaging to wireless data.

Far from slowing down, Innovation continued with the introduction of smartphones. There were some initial attempts at such devices in the 1990s, but by the early 2000s, RIM had established itself as a market leader in the business community with the Blackberry, which focused on email as its primary use. Then, in January of 2007, Steve Jobs introduced the iPhone. "We are going to… get rid of all these buttons and use this giant screen."14 The iPhone wasn’t a technological innovation in itself, rather a new form factor of several established pieces of technology: computer processing, flash memory, battery storage, touch screen, and operating system. It established a new paradigm for how people interacted with their phones, and connected people to the internet, for information, communication and entertainment, regardless of geographical location.

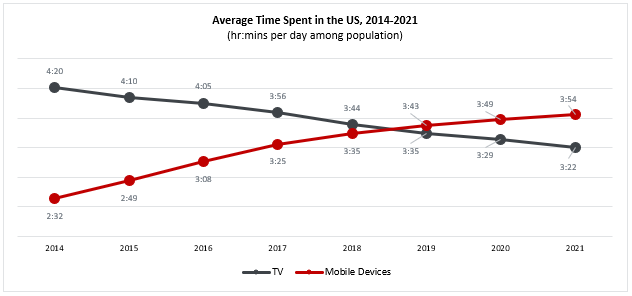

Source: eMarketer April 2019, ages 18+; time spent with each medium includes all time spent on that medium, regardless of multitasking.

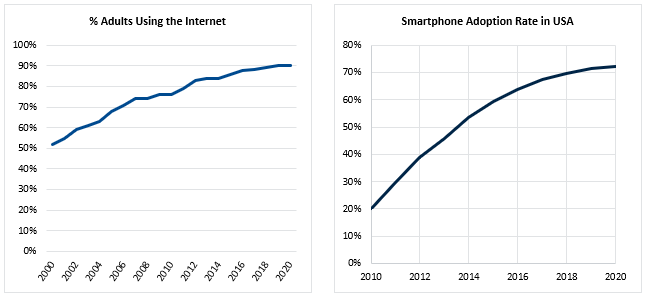

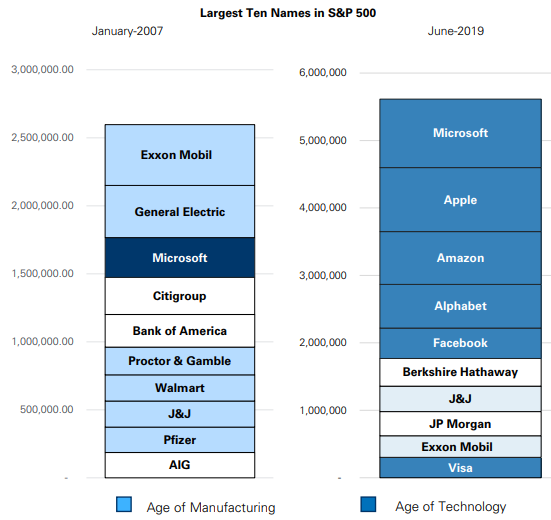

The iPhone first shipped in June of 2007, and with its intuitive interface, the smartphone adoption rate grew significantly, from 20% to 72% of the US population from 2010 to 2018. Normal market competition ensued, with Samsung releasing a competitive product at a lower price point, and the overall market continued to expand. Blackberry failed to adopt the touchscreen format and started posting quarterly losses in 2012. Smartphone sales finally peaked in 2018, the first year that sales ever declined. To put it in perspective of the market penetration, 18% of the population is aged 14 or under15, meaning almost every adult now has a smart phone. In addition, usage of the devices has increased steadily, where daily iPhone usage surpassed TV for the first time in 2019. At almost four hours a day, the average person spends more than a full day on their phone each week. Over this time, Apple went on to become at one point the most valuable company in the world, and the number one contributor to Growth outperforming Value from 2007-2018.16

Value investing generates excess return by an over-discounting of future earnings relative to trailing earnings. But it requires a stabilization and recovery, alongside a rerating of valuations to the new expectations. A good example is Seagate Technology, which a number of short-sellers openly bet against in 2013. The investment thesis was that the PC market was declining with the advent of mobile computing and cloud computing, hard disk drives would be in structural decline. What wasn’t accounted for was that hard disk drives were still the best solution for large scale data centers, so demand would not decline as far as predicted. The stock began 2013 with a P/E around 4x, and price went on to more than double over the next two years through a rerating back to a P/E of 14x17. Seagate’s story is not yet complete, but those two years squeezed the short-seller while the Value investor was rewarded.

Blackberry looked increasingly like a Value investment in the middle of its creative destruction. The P/E ratio of Blackberry company after the iPhone launch reached as low as a P/E in the 3x range until earnings went negative in 2012. Technology revolutions work through creative destruction, which in the case of Blackberry, offers no stabilization for the rerating to occur. OSAM mitigates the risk of Value traps by using quality factors to confirm the health of the company, themes like Earnings Growth, Earnings Quality, Financial Strength, Momentum. But even with quality controls, the clustering of innovation from Technological Revolutions creates more potential traps for Value portfolios.

The Turning Point of 2007-2019

A similar sector weighting imbalance also occurs between the Value and Growth portfolios, with Technology stocks belonging to the Growth side. The technology stocks that contributed in Value are those taking advantage of the infrastructure laid starting in the 1970s. We discussed Apple’s ability to revolutionize mobile computing, and Amazon setting the standard of eCommerce, and they are the two top contributors from Technology. Facebook built a social media empire on top of the internet and mobile computing and contributed strongly. The technology companies that laid the infrastructure like Intel didn’t figure into Value or Growth as they tended to be more Core valuations with relative maturity in their business cycle. Microsoft is the only stock from the Irruption phase that remains a top contributor, as it has positioned itself well within the shift to cloud computing through Azure.

While the rise of Technology stocks is a significant component of the reason that Growth outperformed Value over this turning point, about three quarters of the underperformance comes from Financials18. In the Turning Point of the 4th age, a similar negative impact came from Utilities, so it becomes useful to understand the impact of these sectors on the Value portfolios.

Two Crashes of Financial Capital

Although not well known, Samuel Insull might have had more effect on the utilities industry than anyone else in the country. Insull was originally hired as Thomas Edison’s personal secretary and had risen to become the number three person at General Electric by 1892. At the age of 32, he left to take over Chicago Edison which was about 2% of the size of GE. At Chicago Edison, he established several business paradigms for utilities that exist in today’s utility markets, including the use of AC/DC in distributing power.

As he built out the utility business, Insull aggressively purchased several other utilities, creating a gas and electric empire extending over thirty-two states. The basis for his ability to purchase so many companies was a pyramid holding company structure that heavily favored bonds and preferred stock with a guaranteed dividend. His aggressive acquisition spurred others to similar action, resulting in “eight holding companies controlling 73 percent of the investor-owned electric business.”19 As cash dried up, Insull also switched from cash dividends to stock dividends, using the inflated stock valuations in lieu of cash to keep the machine going. After a takeover attempt, Insull created two additional layers of holding companies to try and retain control. Stacking these structures created massive amounts of leverage, to the point where he controlled an empire of $500m in assets with only $27m in equity20. This leverage was fine in the upmarket, but a market decline would cause significant problems. When asked in a Forbes interview about the leverage in his holding company, Insull responded that “a slump or calamity that would be disastrous [for electric utilities] is practically inconceivable”21.

During the decline of the Great Depression, Utility revenues did hold up better than manufacturing, but even a slight decline caused significant pressure on the company. Insull’s company had pledged its stock as collateral to New York banks, and eventually the company went under when England announced that it was leaving the gold standard. As the banks started uncovering the issues with leverage, the state initiated criminal proceedings, and Insull immediately fled the country, believing there was no way he could get a fair trial. He was eventually extradited and faced trial but was exonerated on all charges. One juror that had served as a sheriff commented he had "never heard of a band of crooks who thought up a scheme, wrote it all down, and kept an honest and careful record of everything they did."22

The criminal system might have determined Insull wasn’t culpable, but the political process did not, resulting in the federal Securities Act of 1933, Securities Exchange Act of 1934, and the Public Utility Holding Company Act of 1935. The last act broke up the holding companies, and forced them to register with the SEC. In addition, the companies were ordered to specialize in one service (such as gas or electricity), and divest all unrelated holdings. This era of tighter regulation created a barrier for utility companies in achieving economies of scale and generating supernormal earnings for the foreseeable future.

We don’t need to revisit the Financial crisis, so long as the reader understands the similarities to what happened with Utilities from 1926-1941: the belief that a market would never go down, combined with leverage, led to a bubble and subsequent collapse, which was followed by public outrage and tighter regulation.

Carlota Perez’s model accounts for both of these collapses in Part II of her book, where she introduces the relationship between financial capital and production capital. As the Frenzy and Turning Point part of the cycle occurs, the success from investing causes financial capital to “believe itself capable of generating wealth by its own actions, almost like having invented magic rules for a new sort of economy23.” In this case, the leverage used from Insull’s scheme, and the easy money from subprime credit, both fueled by the belief that the demand for electricity and housing prices would never collapse.

Furthermore, the impact of those stocks was almost completely contained to stocks with cheap Valuations. As the market sensed the distress from these two sectors, Valuations dropped creating Value traps as the earnings fail to recover.

Moving Along the Curve

Hopefully by this point we have established that while this may be a long-term market dynamic, the last twelve years are something we have gone through before. There are periods of innovation clusters that change the standards of our society, the consumption patterns of the economy and how the value from those economic actions are distributed across public companies. These clusters of innovation have periods of transition from widespread Installment to Deployment are aligned with regimes when Growth outperforms Value. The insight provided by this analysis is that as the economy transitioned out of the turning point to the Deployment phase, the economy enjoyed broad growth from the expanded utilization of the framework, during which Value returned to outperforming growth. There is no guarantee this pattern will continue, but the rationale is compelling.

Looking at the 4th Technological Revolution, we can see that Value Investing returned to form fairly quickly as we moved along to Deployment and the high growth of Synergy. All three Value factors generated higher spreads within that period than across the entire 92-year period. The chart showing the decline for Price-to-Book across the two periods looks remarkably similar, and one can see the sharp rebound starting in 1942.

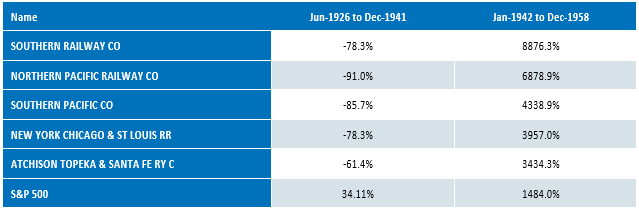

Attribution of the Synergy phase of 1942-1959 shows that some of the outperformance came through Manufacturing as companies like Goodyear Tire, Texas Co and International Paper moved to from Growth to Value, similar Apple moving towards Value (based on earnings) over the last few years. But the main contributor to Value outperforming was from railroads and utilities, the companies of the third Technology revolution that dragged so badly during the turning point of 1929-1941. The railroad industry began a transformation from Steam to Diesel in the 1930s, moving away from the Third revolution and fully into the Fourth. This change dramatically changed their cost structure, where dieselized railroads created a competitive cost advantage over trucking for mass transport of goods. Southern Railway, the railroad with the strongest returns over this time period, started adopting diesel in 1939, and became the first major carrier to have a complete diesel fleet by 195324.

If we believe that this long-term historical narrative will play out, the important question is when are we moving into the Deployment phase? For allocators of capital, we want to know how much longer this Growth Regime can last.

We do have the timing mechanisms of the market crashes. The problem is that there is no prescribed passage of time after the bubble correction when you move into Deployment. That said, given that it’s been twelve years, it certainly seems like this period is getting a bit long in the tooth.

One key pivoting point in any technology is when the standards is set for how the technology will be deployed across society. In the case of technology, one could argue that the introduction of the smartphone disrupted the consumption patterns of information, and we are still figuring out the matching of platform to consumption. The societal habits for whether people will use their desktop, laptop, gaming console, smart speaker, tablet or phone for communicating, shopping, gaming, and business productivity. But with the smartphone adoption curve shown before, the platform is established for delivery of information to anyone anywhere, and with embedded cookies, canvas fingerprinting, and geolocational tracking, the delivery of information on everyone to anyone.

Another key sign in standards being set are the formation of oligopolies and monopolies. For every one of the previous technological revolutions, there have been winners that have established the standards accumulated market share and became synonymous with the technology itself. The chart below shows the shift in the market leadership over the last twelve years, with the Age of Technology forming oligopolies through the FAANG stocks.

It should be mentioned that because these oligopolies are so large, one would suspect that they can’t get bigger. Amazon’s market share is 49% of online retail and 5% of total retail. While it’s one of the largest companies in the world, there’s still potential to grow. Sears didn’t grow to become 1% of GDP until the 1950s, well into the Deployment of the cycle. General Motors and Sears were the top two contributors to the Growth Portfolio25 during the synergy phase of 1942-1959, but the Value portfolio outperformed during the creative construction of deployment, where the overall economy grew and the value cycle of stocks being overly discounted and rerated was the norm.

One should not underestimate the role of regulation in how the Age of Technology plays out. The recent Senate hearings on Facebook highlight that privacy rights are far from established and could create structural issues for technology companies. Additionally, anti-trust legislation always rears its head as near monopolies exert power.

If Value investors take nothing else from this piece, hopefully it gives perspective. Technological revolutions are one framework for looking at history, but they offer a lot of insight into what our world and our markets are going through right now. The introduction of the internet and mobile computing has been broad and swift, introducing change at a far greater pace than the automobile. And it makes sense that these changes will cause distress on businesses from the previous paradigm. These are long cycles that have played out before, starting with the Industrial Revolution in the 1770s. What we have offered here, as our ability to gather historical data continues to improve, is the possibility that long regimes where Growth outperforms Value are part of these arcs. We have also seen that eventually as the innovations move to maturity, Value investing has also returned towards a longer-term trend of outperforming.

Thank you to Jamie Catherwood for his help with the historical research, particularly on Railroads, Utilities and Automobiles from the 1920s and 30s. Daniel Nitiutomo helped with the attribution calculations for the historical S&P 500 portfolios. Travis Fairchild assisted with data collection for the OSAM Deep History. And last, thank you to Jamie, Ari Rosenbaum and Patrick O’Shaughnessy for editorial comments.

Appendix A – OSAM Deep History

The OSAM Deep History dataset was created through several steps. OSAM procured digital copies of the entire history of Moody’s Manuals for Transportation, Industrials and Railroads. A list of companies available through CRSP with a market cap over $200m (inflation-adjusted) and a stock price over $1 were supplied as the companies to generate data for. These files were sent to an offshore third party, where the entirety of the income statement and balance sheet were typed into spreadsheets.

In order to determine which items were Sales, Net Income and Book Value of Equity, a supervised machine learning algorithm (Support Vector Machine) was used. We classified about 5% of the data manually and used those as the training data set. Any items with sufficient confidence level of classification was incorporated into the dataset. Another round data entry was performed to get almost 100% coverage of S&P index constituents. A data outlier algorithm (Isolation Forest) was used to look for additional outliers within the data, which were subsequently cleansed.

Appendix B – Value Portfolios

For the investment universe we limited ourselves to the S&P 500 constituents available through CRSP. The idea was for 1) an investible universe of stocks so the research would reflect real world conditions and 2) have our methodology be replicable to other researchers could verify findings. The S&P 500 constituents became 500 stocks in 1957, so from 1926 to 1957 there are only 90 stocks in the universe for investment.

Pricing and market capitalization are provided by CRSP. Sales and Net Income were sourced from OSAM Deep History and Compustat, with Deep History being the primary source for fiscal years of 1956 and before, and Compustat thereafter. Book Value was sourced primarily through Compustat, followed by the dataset provided on Ken French’s website, and lastly through the OSAM Deep History. The reason for using Ken French’s data for Book Value first was to allow for replication of the time series on Price-to-Book by others.

Portfolios are formed using a similar methodology as Fama-French (1993), fundamentals are formed at the end of June every year to ensure full reporting of annual reports. This also coincides with the release of the Moody’s manuals the new dataset is based on, to ensure there is no lookahead bias.

Because of the limited number of stocks in the universe, we build Value and Growth portfolios based on the Fama-French 1993 methodology of Top 30% and Bottom 30% for each valuation metric. This ensures an appropriate number of stocks in each portfolio to achieve diversification of stock-specific risk. We use value-weighted (i.e. market-cap weighted) returns for each test. Equally-weighted returns of S&P 500 constituents were also run, and showed similar underperformance during the time frames discussed.

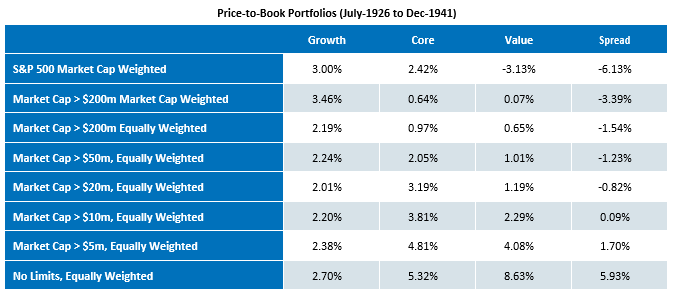

One note: while our S&P 500 portfolios aligned generally with the Value-Weighted portfolios on Ken French’s website, we saw significant differences in the equally-weighted universes. We believe this is due to the inclusion of microcap stocks in the French portfolios. The following table shows the returns on the 30/40/30 portfolios formed on Price-to-Book using various market cap limits (inflation adjusted) for the 1926 to 1941 time period. The inclusion of a small number of very small companies dramatically shifted the equally-weighted Value portfolio. This is particularly true in 1932, where small companies like the Manati Sugar Co, with a total market capitalization of thirty-one thousand dollars, was up 800% over the next twelve months. We believe including these companies provides an inaccurate representation of how Value investors would have done from 1926-1941.

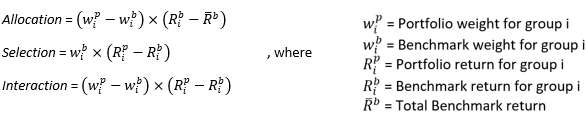

Appendix C – Attribution Calculation

In this paper, a multi-period Brinson Attribution methodology was applied to account for relative performance contributions. For every period, group weights, returns and contributions were calculated for each portfolio. The relative performance for every group was then decomposed into Allocation, Selection, and Interaction effects following the Brinson approach:

Portfolio contributions and relative performance decompositions were linked across periods using a geometric linking method. Group allocation, selection, and interaction effects were then summed to arrive at total effects. The residual of actual excess performance and linked excess performance was distributed equally across all final composed effects.

Footnotes

1 See Appendix A on the data collection methodology

2 Broad SIC classifications were used to define sectors. Using two-digit codes, Manufacturing is 20-39, Utilities are 40-49, Financials are 60-69, Technology stocks are predominantly in code 73.

3 Note: the Utilities sector includes power Utilities such as Gas and Electric, as well as Railroads

4 Also known as Kondratiev waves, first observed by Nikolai Kondratiev in “Major Economic Cycles” (1925)Gas and Electric, as well as Railroads

5 P.71, Perez

6 P.274, “As Time Goes By”, Freeman and Louca

7 P.275, “As Time Goes By”, Freeman and Louca

8 OSAM Research. Source: Number of Firms Participating in the Auto Industry in the U.S.: Utterback, JM, and FF Suarez. “Innovation, Competition, and Industry Structure.” Research policy. December (1993)

9 Note: Ford was a private company until 1958. Value based on Price-to-Book.

10 P.265, “As Time Goes By”, Freeman and Louca

11 P.289, “As Time Goes By”, Freeman and Louca

12 https://www.theatlantic.com/business/archive/2017/10/amazon-sears-mistakes/541926/

13 OSAM Research

14 P.129, Losing the Signal, McNish, Silcoff (2015)

15 https://en.wikipedia.org/wiki/Demography_of_the_United_States

16 Note: Apple was in the Growth portfolio for Price-to-Book for almost the entirety of 2007-2018, but was not consistently in the Growth portfolio on Earnings. By the middle of 2013 it actually moved into the Value portfolio, and is a contributor for the difference in performance between P/B and P/E over that time period.

17 OSAM Research

18 The impact of financials is slightly higher in S&P 500 portfolios because it is using just the top 30% and bottom 30% on on Price-to-Book, but it’s not far off from contribution for the Russell 1000 Growth and Value, where Financials accounted for about 56% of the total underperformance from Jan-2007 to Dec-2018.

19 Hyman, Leonard S. (1988), America's Electric Utilities: Past, Present and Future, Public Utility Reports, p. 74. As cash dried up, Insull also switched from cash dividends to stock dividends, using the inflated stock valuations in lieu of cash to keep the machine going.

20 https://www.nytimes.com/2006/03/19/business/yourmoney/before-there-was-enron-there-was-insull.html

21 P.59 “From Insull to Enron”, Henderson and Cudahy, Energy Law Journal, (2005)

22 P.71, “From Insull to Enron”, Henderson and Cudahy, Energy Law Journal, (2005)

23 P.75 Perez

24 https://en.wikipedia.org/wiki/Southern_Railway_(U.S.)

25 Valuation based on Price-to-Book

General Legal Disclosures & Hypothetical and/or Backtested Results Disclaimer

The material contained herein is intended as a general market commentary. Opinions expressed herein are solely those of O’Shaughnessy Asset Management, LLC and may differ from those of your broker or investment firm.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by O’Shaughnessy Asset Management, LLC), or any non-investment related content, made reference to directly or indirectly in this piece will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this piece serves as the receipt of, or as a substitute for, personalized investment advice from O’Shaughnessy Asset Management, LLC. Any individual account performance information reflects the reinvestment of dividends (to the extent applicable), and is net of applicable transaction fees, O’Shaughnessy Asset Management, LLC’s investment management fee (if debited directly from the account), and any other related account expenses. Account information has been compiled solely by O’Shaughnessy Asset Management, LLC, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, O’Shaughnessy Asset Management, LLC has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact O’Shaughnessy Asset Management, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: Please compare this statement with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. Historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. O’Shaughnessy Asset Management, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the O’Shaughnessy Asset Management, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request.

Hypothetical performance results shown on the preceding pages are backtested and do not represent the performance of any account managed by OSAM, but were achieved by means of the retroactive application of each of the previously referenced models, certain aspects of which may have been designed with the benefit of hindsight.

The hypothetical backtested performance does not represent the results of actual trading using client assets nor decision-making during the period and does not and is not intended to indicate the past performance or future performance of any account or investment strategy managed by OSAM. If actual accounts had been managed throughout the period, ongoing research might have resulted in changes to the strategy which might have altered returns. The performance of any account or investment strategy managed by OSAM will differ from the hypothetical backtested performance results for each factor shown herein for a number of reasons, including without limitation the following:

▪ Although OSAM may consider from time to time one or more of the factors noted herein in managing any account, it may not consider all or any of such factors. OSAM may (and will) from time to time consider factors in addition to those noted herein in managing any account.

▪ OSAM may rebalance an account more frequently or less frequently than annually and at times other than presented herein.

▪ OSAM may from time to time manage an account by using non-quantitative, subjective investment management methodologies in conjunction with the application of factors.

▪ The hypothetical backtested performance results assume full investment, whereas an account managed by OSAM may have a positive cash position upon rebalance. Had the hypothetical backtested performance results included a positive cash position, the results would have been different and generally would have been lower.

▪ The hypothetical backtested performance results for each factor do not reflect any transaction costs of buying and selling securities, investment management fees (including without limitation management fees and performance fees), custody and other costs, or taxes – all of which would be incurred by an investor in any account managed by OSAM. If such costs and fees were reflected, the hypothetical backtested performance results would be lower.

▪ The hypothetical performance does not reflect the reinvestment of dividends and distributions therefrom, interest, capital gains and withholding taxes.

▪ Accounts managed by OSAM are subject to additions and redemptions of assets under management, which may positively or negatively affect performance depending generally upon the timing of such events in relation to the market’s direction.

▪ Simulated returns may be dependent on the market and economic conditions that existed during the period. Future market or economic conditions can adversely affect the returns.

Composite Performance Summary

For the full composite performance summaries, please follow this link: http://www.osam.com